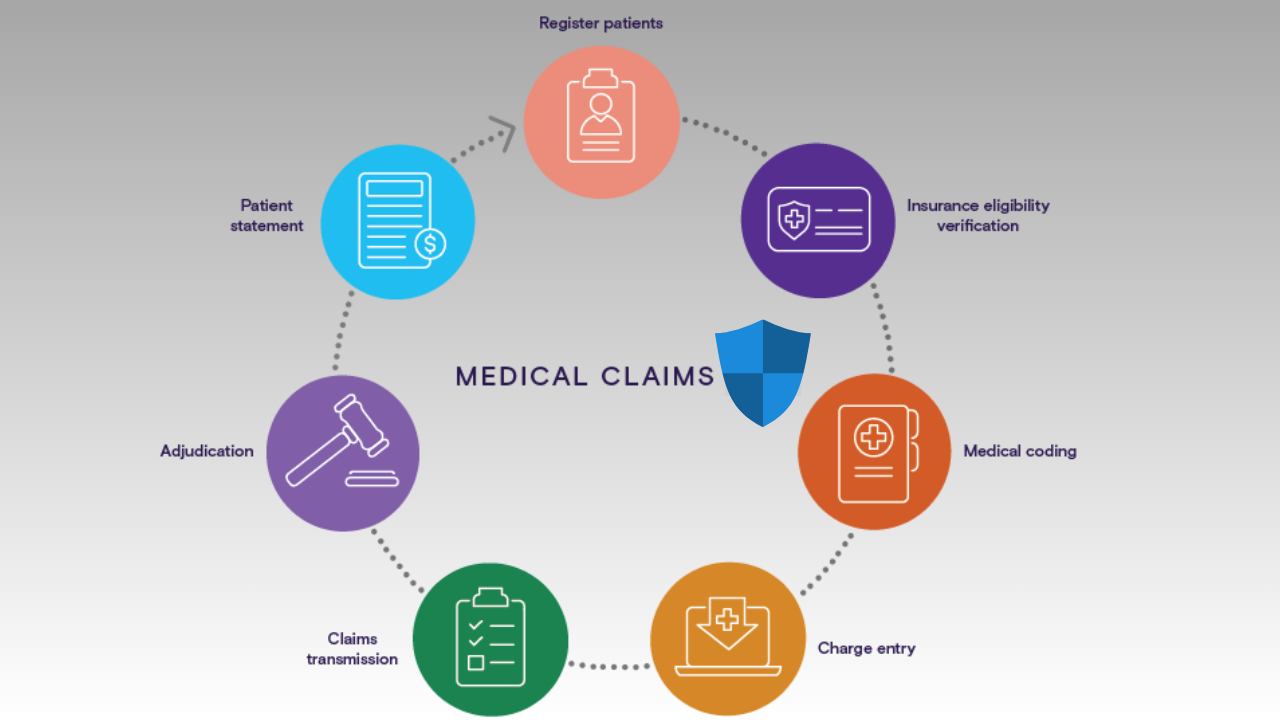

Health Insurance Claim Settlement is the method involved with asserting your health care coverage strategy benefits from the insurance agency. At the point when you purchase health care coverage, it accompanies a cover as a total protected. The aggregate safeguarded is used to give monetary guide in the event of crisis/coincidental hospitalization/clinical treatment costs.

How would you use your total safeguarded? By making a case straightforwardly with your guarantor. Upon fruitful enlistment of your case, the guarantor will in like manner repay the expense of clinical treatment caused.

For instance, Mr. A met with a sad mishap for which he was confessed to the emergency clinic for 48 hours. The expense of clinical treatment, specialists’ charges, and the emergency clinic bill came up to Rs. 1 lakhs. Since Mr. A has an exhaustive health care coverage inclusion strategy of up to Rs. 5 lakhs aggregate protected, he can rapidly settle this case with his insurance agency. Under this interaction, how much Rs. 1 lakh will be repaid to Mr. A by his insurance gives, according to the contract cover.

As referenced over, the two most normal strategies for making a case are through credit only or repayment mode.

What are the Types of Claim Settlement Options?

There are two types of claim settlement options:

1). Cashless Claim Settlement Option

A credit only case choice must be profited in the event that you are owned up to an organization emergency clinic, as referenced in the strategy report. Your strategy report has a rundown of organization clinics in your city of home. With the credit only mode, you really want not pay a solitary sum from your wallet. The back up plan will take care of the whole expense of hospitalization and clinical treatment. You should simply outfit your credit only wellbeing card to the outsider overseer.

2). Reimbursement Claim Settlement Option

Under this choice, you will be expected to cover the emergency clinic bill and cost of clinical treatment to the clinic, quickly post-treatment or before release. Then you want to petition for guarantee repayment straightforwardly with your safety net provider. The back up plan will repay the expense of treatment according to the approach phrasings.

What are the Documents Required for Claim Settlement Process?

All the listed documents should be original:

Copy of Health Card

Copy of FIR in case of an accidental emergency

Hospital discharge card

Invoice for medicines

Original medical bills and scripts

investigation/diagnostic reports/X-Ray

Treatment papers

Doctors’ prescription

Certificate from attending doctor/physician stating the condition of the patient

Relevant Investigation reports (Radiology, Pathology, etc) confirming the diagnosis

Consultant’s certificate with diagnosis (including the date when symptoms first occurred)

KYC – PAN card and Hospital Registration Card

Cancelled cheque

Claim application Form – Duly filled and signed

How to Make a Health Insurance Claim?

Visit the network hospital of your choice

The TPA will coordinate with your insurer for a pre-authorization form

Submit your cashless card at the TPA

Submit the relevant documents required for treatment

Post verification, the insurer will grant the precision for covering the cost of treatment meant

Make sure you take all the records of your treatment and hospital bills

In the reimbursement mode case, you will be required to clear the hospital bill from your own pocket. Later, when you are discharged, you will have to file a reimbursement claim with your insurer along with the relevant documents. Post submission, your insurer will process the claim accordingly and reimburse the treatment cost straight to your account.

Fill the Cashless Request Claim Form and submit the same to the TPA

Ensure that you have a relevant photo ID and policy number

Claim settlement process via cashless mode/pre-planned:

Why Insurance Claim Get Rejected?

You can also check here.

Here are the instances under which your claim can get rejected:

Any fraudulent claims

Claim under an expired policy

Treatment which is not covered under the scope of cover

Treatment within the waiting period

All types of general and standard exclusions

How to Claim Health Insurance Under Multiple Insurers

It is feasible to have a singular health care coverage plans as well as a gathering insurance contract from your boss. Regardless of whether you have two wellbeing plans from private guarantors, the inquiry in regards to documenting a case under various safety net providers could confound you. For this situation, you should raise a protection guarantee with the primary insurance agency for the costs caused and get a synopsis of the case settlement. Then, at that point, you can present this report to the second back up plan to get the excess pay. The interaction might contrast starting with one protection supplier then onto the next and hence, it is urgent to know the case settlement strategy appropriate to your safety net providers.

Claim Settlement Ratio in Health Insurance

Guarantee Settlement Proportion or CSR is a viewpoint that is thought about while picking a reasonable health care coverage supplier. In straightforward terms, CSR lets you know the likelihood of your protection guarantee getting gotten comfortable what’s in store. The Case Settlement Proportion is assessed by taking the all out number of cases settled by the organization against the all out number of cases got in a specific year. You can without much of a stretch work out this figure to look at and pick a reasonable safety net provider. It is encouraged to choose an insurance agency with a high Case Settlement Proportion.

Common Reasons for Health Insurance Claim Rejection

There are times when your health care coverage guarantee could get dismissed by the back up plan however what could be the reason? Here are a few normal motivations to remember that lead to guarantee dismissal:

Non-Disclosure of Medical History

One of the vital purposes behind guarantee dismissals is the inability to uncover your clinical history while buying the protection plan. Concealing any previous circumstances that you could have isn’t suggested as protection plans don’t cover such infirmities without a holding up period.

Providing Incorrect Information

Giving incorrectly subtleties while purchasing health care coverage, for example, your age, occupation, family clinical history, pay subtleties, and so on can be one more justification for guarantee dismissal. In addition, insurance agency could likewise end your approach for giving incorrectly data.

Claim Falls Under Exclusions

Each wellbeing strategy has a bunch of rejections connected with medicines or problems that are not covered by the back-up plan. On the off chance that your clinical protection guarantee falls under the rejections referenced under your arrangement, the clinical consideration costs won’t be repaid by the organization.

- Passed Insurance Contract

Assuming your wellbeing strategy has terminated or slipped by, the protection supplier won’t cover any medical services costs brought about. Regardless of whether the case is recorded during the effortlessness time frame, no costs will be repaid.

Raising a Claim During the Waiting Period

For explicit sicknesses, add-on covers or previous circumstances, a holding up period is relevant under the wellbeing plan. In the event that any case is recorded during this period, the safety net provider won’t cover it as the holding up period isn’t finished.

Tips to Make a Successful Health Insurance Claim

To make sure you can raise a successful health insurance claim, you must note these tips!

- Understand the exclusions, and terms and conditions applicable to your plan.

- Maintain the original bills and invoices along with diagnostic and investigative reports.

- Know the waiting period applicable to your insurance policy.

- Intimate the insurance provider regarding the claim at the earliest.

- Follow the claim intimation conditions and time durations while raising an insurance claim.

- Fill the claim settlement form accurately without any errors.

- Ensure to fill the health insurance application form yourself.

- Avoid hiding any details and disclose your past and current medical history while buying insurance.

Important Pointers to Remember While Filing Health Insurance Claims

There are numerous terms and conditions associated with your health insurance that you must know while raising a claim. Not being aware of these aspects can lead to unnecessary out-of-pocket expenses or even rejection of a claim.

- The inclusions and exclusions under your health insurance policy, particularly about hospitalisation

- Room rent limits mentioned in your health plan

- The minimum waiting period for specific conditions or treatments

- The co-payment clause

- The sub-limits for various covers under your health insurance policy

When you are looking to buy a health plan, ensure that you go for a company with a high claim settlement and incurred claims ratio.

Authorisation Process for Health Insurance

The insurance provider verifies the coverage and policy details of the insured as soon as they receive claim intimation from the policyholder and the network hospital. A field doctor is then assigned who shall handle the pre-authorisation process and review the medical treatment. Upon verification, the insurance company will approve the cashless health claim based on the terms and conditions of the insurance plan.

How to Check the Status of Health Insurance Claims

- For Cashless Claims: You can check the status of cashless health insuranceclaims at the insurance help desk in the hospital. The process will be initiated there and you will be informed of the deductibles to be cleared as well.

- For Reimbursement Claims: For the status of your reimbursement insurance claim, it is recommended to reach out to your insurance provider. You can contact them via their toll-free number or their email ID

Conclusion

We trust that you have perceived health care coverage claims exhaustively and figured out how to guarantee clinical protection. To avoid guarantee dismissals and capitalize on your protection inclusion, abstaining from concealing anything from your protection provider is encouraged. In spite of the fact that you could profit a lower premium statement by not unveiling prior conditions or way of life propensities before all else, it will just prompt case dismissals later on. Furthermore, your protection inclusion will miss the mark in getting your wellbeing necessities.

Yet, have you been postponing buying protection up to this point? Peruse the health care coverage anticipates Bajaj Markets to acquire broad inclusion and safeguard your funds against taking off medical services costs!

At the point when you are hoping to purchase a wellbeing plan, guarantee that you go for an organization with a high case settlement and caused claims proportion.

Authorisation Process for Health Insurance

Check Here Details: https://health.policybazaar.com/

The insurance supplier checks the inclusion and contract subtleties of the protected when they get guarantee insinuation from the policyholder and the organization medical clinic. A field specialist is then doled out who will deal with the pre-authorisation cycle and survey the clinical treatment. Upon confirmation, the insurance agency will support the credit only wellbeing guarantee in view of the agreements of the protection plan.

How to Check the Status of Health Insurance Claims

- For Cashless Claims: You can check the situation with credit only medical coverage claims at the protection help work area in the emergency clinic. The cycle will be started there and you will be educated regarding the deductibles to be cleared too.

- For Reimbursement Claims: For the situation with your repayment protection guarantee, it is prescribed to contact your protection supplier. You can reach them through their complementary number or their email ID

Commonly Asked Questions

- I have quite recently purchased a health insurance plan. Am I entitled for the credit only treatment?

- Each health Insurance plan entitles for the credit only treatment gave you look for it in a clinic that is inside the organization of the insurance agency. As referenced before, at least 24 hours of hospitalization is obligatory to guarantee on your health care coverage

- Q. Imagine a scenario where the insurance agency deny my solicitation for credit only treatment.

- • According to the IRDAI rules, no guarantor can deny your legitimate case. Subsequently, assuming your solicitation for the credit only treatment is denied because of substantial reasons, you can in any case pay towards the treatment and all connected costs through your own pocket and afterward raise the solicitation for repayment. In the event that your case demand is inside the extent of inclusion according to the arrangement agreements, it can’t be dismissed

- What are the charges/expenses that are not canvassed in the health insurance plan?

- There are sure costs that are not canvassed in any medical coverage plan, for example, regulatory charge, administrations charge, costs connected with clothing, additional bed, toiletries, diapers, needles, phone charges, and so on. For itemized data on whats not covered by your insurance agency, if it’s not too much trouble, allude the strategy phrasings

- Is there any holding up period to guarantee on my health care coverage?

- Commonly, every health care coverage strategy is packaged with three kinds of holding up periods.

- The underlying holding up period: This determines to an underlying 30 days of holding up period where you can’t raise a case on your wellbeing strategy besides in the event of a mishap.

- Illness explicit holding up period: There are sure infirmities that are covered by the wellbeing strategy solely after a specific holding up period like two years. This rundown differs according to insurance agency and is referenced in the approach phrasings.

- Prior Illness holding up period: Most insurance agency cover the previous infections after a holding up time of 3-4 years. Subsequently, in the event that you have determined any ailment as prior during the hour of strategy buy, a similar will be covered solely after the holding up period referenced in your approach

- Q. What is guarantee stacking in health care coverage?

- Guarantee stacking is the sum charged by the medical coverage organization on your restoration expense when you make claims in your strategy. Most medical coverage organizations contain stacking in their arrangements. There are various manners by which stacking is determined by the undertakings